Buhlmann's Corner

Two sides of the same coin

A board of management is held responsible for everything and, in accordance with the principle of first among equals, its chair that much more so. Obviously the incumbent does not attend to the nuts and bolts of everything in person, but the totality of scope in organisational detail comes with totality of responsibility for it as a whole.

A board of management is held responsible for everything and, in accordance with the principle of first among equals, its chair that much more so. Obviously the incumbent does not attend to the nuts and bolts of everything in person, but the totality of scope in organisational detail comes with totality of responsibility for it as a whole.

And so, as was the case of Rupert Stadler (AUDI) for whom the penny didn’t drop until several months after his arrest for fraud, accountability is as vital to responsibility as is a flame is to a moth, German accountables took to dancing in the street when on July 1 1994, Germany introduced D&O insurance (directors and officers). To offset the onus of responsibility, they can demand astronomically high salaries and highly respectable retirement packages which, to all intents, shifts liability to the insurance and reinsurance companies. A measure akin to this had begun to emerge in late 19th Century Prussia only to be quashed by the Minister of the Interior, vehemently opposed to the introduction of insurance of such low morality.

Today, the only detail of interest contained in legal codes and directives is the volume of minimum exemption thresholds. Management board members must abide by rules that cover “all that stuff” that asset managers must perform in order to forestall liability, consult one of the two major vote recommendation agencies and, just to be on the safe side secure the services of both directly – recommendations tend to be the same anyway.

The only time that their real business – getting paid for freeing asset managers from liability – becomes complicated is when managers do things that the famous rules have not (yet) got round to dealing with. Why on earth should asset managers have to take on any more decision making than what their daily job of investing and disinvesting requires of them. They are the watchdogs who invigilate over the board of management and the Supervisory Board as to whether they act within the terms of the rules of the state and hence the law of the land. This being the case, problems inevitably arise when the mere two-thirds of those entitled to vote are present at a company AGM and this is deemed sufficient, or the fact that nobody registers surprise when the number of those registered as attending a company AGM turns out to be twice the number of those actually there.

An example of responsibility is DEKA when it sues Volkswagen. If DEKA wins the case every Volkswagen shareholder pays damages to DEKA from their share portfolio.

They had only to dig deeper beforehand and then vote for and/or appoint the best of a better selection. The case took a grotesquely twisted turn when the main actor, the CFO, was promoted to chair the Supervisory Board, the slant being “best not to know”. As regards organisational performance and managerial skills, the management board pocketed huge sums of money and lost no sleep over withholding knowledge of wrongdoing. Assuming the rumours are true, the Asset Manager sent the proxies and the liability purchased by ISS & Glass Lewis, without verifying where they ended up (requesting a receipt for votes cast perhaps?). Out of sight, out of mind.

But it was accountability itself that rubbed salt into this wound. In Germany, article 2 of the directive on shareholders’ rights amended § 129 Abs. 6 of the law on shares traded on the stock market that gives all shareholders the right to know how their votes were cast. The answer comes in the form of an observable technical function and too late to be of any use when the votes have gone abroad. Responsibility nil liability nil, Game over.

In Germany the so-called Energiewende, which, if the truth were told was nothing short of unconstitutional confiscation had been continually postponed so that the issuers– today known autility companies – reorganize. Yes, indeed, reorganize because outside the actual companies, all the asset managers had done was promote a bit of light marketing in populist tones raising a half-hearted protest instead of defending the company as a benchmark of sustainability and reference point for co-determination.

The list of sad examples was not limited to E.on and RWE, Volkswagen or Daimler, but included Deutsche Bank and its wobbly cultural turnaround, and lately Thyssenkrupp too. Hand in glove wih its scientist chair the board of management still needed more time to turn the company inside out, in or counter to shareholders’ interests even after the heads had stopped rolling. Right of appointment introduced in 2007 was at its most costly. Erich SIXT head of his own family stock market traded auto leasing group abolished it with no replacement.

In the end, the first market for D&O insurances was the USA, introduced contemporarily with the infamous Wall Street crash in New York on October 25 1929, Black Friday. The slump that followed brought bankruptcy to a great many banks and companies.

Verantwortung und Haftung

2 Seiten einer Münze

Jeder Vorstand trägt Gesamtverantwortung, der Vorsitzende am stärksten nach dem Grundsatz pars inter pares. Zwar fräst und dreht er nicht jede Schraube selbst, aber über das Institut der Organisations-Verantwortung ist er dran. Und im Zweifel merkt er dann – wie Rupert Stadler (AUDI) – erst weit nach seiner Verhaftung, dass die Haftung zur Verantwortung gehört, wie die Fliege zum Licht.

Genau deswegen haben die Haftenden vor Freude gejohlt, als nach dem 1.7.1994 die D&O Versicherung in Deutschland heimisch werden konnte. Für die Last der Verantwortung konnte man nun hohe Gehälter und dicke Pensionen kassieren und die Haftung dabei in das Netzwerk der Erst- und Rückversicherer fallen lassen. Ende des 19. Jahrhunderts war das schon einmal in Preußen erörtert worden, doch das Preußische Innenministerium wies dieses unmoralische Versicherungsprodukt damals ab.

Nun werden in den Leitlinien und Kodizes nur noch die Selbstbehalte als ganz wichtiges Detail diskutiert. An diese Regularien müssen sich Vorstände halten, denn hier ist auch „alles“ geregelt, was die anlegenden Asset Manager zur Verhinderung ihrer Haftung tuen: sie beauftragen eine der beiden globalen Abstimmungsempfehlungs-Agentur und um ganz sicher zu gehen, kaufen sie die Deckung gleich bei beiden ein – Unterschiede bei den Empfehlungen sind sowieso eher selten. Schwierig ist deren Geschäft – dem Asset Manager die Haftung gegen Geld wegzunehmen - höchstens dann, wenn Vorstände etwas tun, was im Regelwerk (noch) nicht vorgesehen war.

Photo: VIPsight

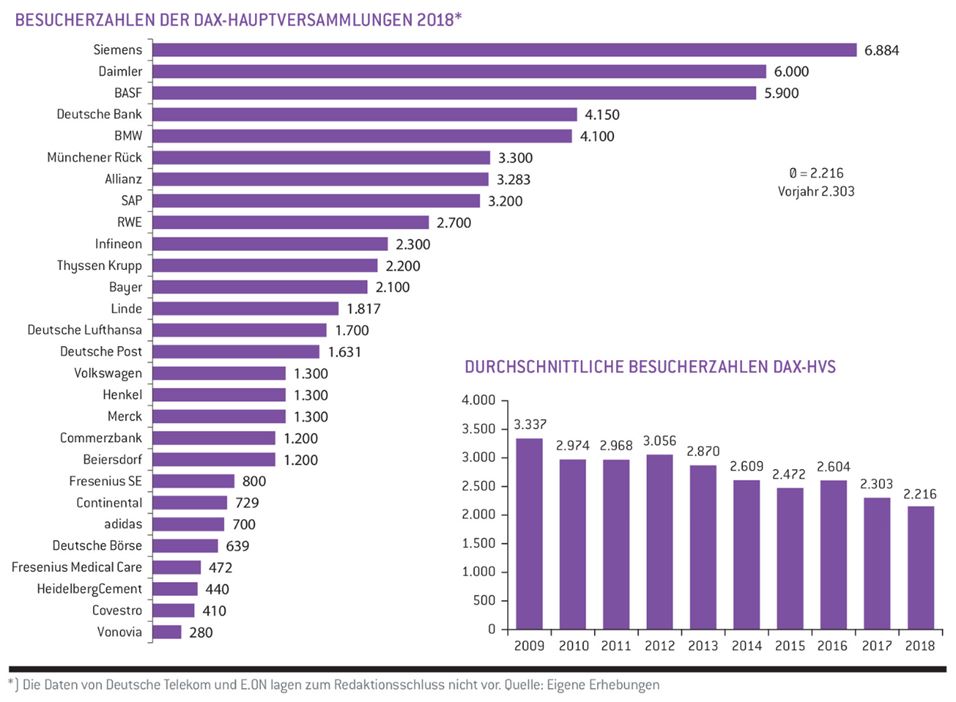

Wieso tragen Asset Manager überhaupt Verantwortung (hier abgesehen von deren Auswahl der zu des- /investierenden Gattung)? Sie müssen die Vorstände (und Aufsichtsräte) mit den Werkzeugen der staatlichen Regelwerke (Gesetze) kontrollieren. Da bleibt es schon erstaunlich, dass mit Hauptversammlungs-Präsenzen von 2/3 aller Aktienstimmen Zufriedenheit einkehrt – oder gar mit Präsenz-Ergebnissen von über 100% nur ein Achselzucken erzeugt wird.

Verantwortung zeigt zum Beispiel die DEKA durch eine Klage gegen Volkswagen. Sollte DEKA den Streit gewinnen, zahlen alle Aktionäre des Emittenten den Schadensersatz der DEKA aus dem gesamten Aktionärsvermögen. Die hätten ja vorher aufpassen und vielleicht bessere Manager wählen und bestellen können. Da bleibt es ein Rülpser der Geschichte, wenn der Haupttäter Finanzvorstand zum Aufsichtsrat-Vorsitzenden befördert wurde.

Grafic: HV Magazin Sonderausgabe Locations 2018/19 http://gp-mag.de/hvloc1819

Am Schönsten ist dann immer noch „nichts gewusst“ zu haben. Der Vorstand hat wegen seiner Organisationsleistungen und Managementkompetenz zwar heftig kassiert, lässt sich aber von keinem Schuld begründenden Wissen am Nachtschlaf hindern. Der Asset Manager hat (wenn überhaupt) sein Stimmrecht mit der gekauften Verantwortung von ISS & GlassLewis auf die Reise gegeben, ohne nach einer Quittung zur Stimmrechtsausübung zu fragen: was man nicht weiß, macht einen nicht heiß. Und heiß steht hier für verantwortlich. Hoppla, da regelt das (deutsche) Einführungsgesetz der 2. Shareholder Rights Directive einen neuen §129 Abs. 5 AktG, wonach jeder (!) Aktionär ein Quittungsrecht gegen den Emittenten hat – obwohl das spätestens cross border technisch gar nicht funktionieren kann. Verantwortung weg, Haftung weg und Ruhe ist.

Die so genannte (deutsche) Energiewende, die nichts anderes als eine entschädigungslose (also verfassungswidrige) Enteignung der Aktionäre darstellte, konnte über Jahre verschleppt werden, bis dann die Emittenten –die so genannten Versorgungsunternehmen - sich neu sortiert haben. „Neu sortiert“ ist schon der zutreffende Passus, denn von außerhalb der Emittenten kam es maximal zu einem marketinggetriebenen Einsatz der Asset Managern, die dem Populismus aufs Maul geschaut, zu mäßiger Kritik aufgelaufen sind, anstatt den nachhaltigen Unternehmenswert als Maßstab und Richtschnur für Ihre Mitbestimmung anzusetzen. Schlimme Beispiele sind nicht nur E.on und RWE oder Volkswagen und Daimler, auch die Deutsche Bank mit ihrem immer noch quietschenden Kulturwandel und jüngst Thyssenkrupp. Nachdem die Köpfe entnervt gefallen und weggerollt wurden hat es ein wenig gedauert, bis ein Vorstand Hand in Hand mit seinem wissenschaftlichen Vorsitzenden mit, den Konzern gegen oder für die Aktionäre von den Füssen auf den Kopf gestellt wurde. Das 2007 erschaffene Entsenderecht zeigt ich von seiner teuersten Seite – da freut es, wie Familien-Unternehmen (und –Unternehmer Erich) SIXT das Entsenderecht 2018 ohne Gegenleistung bei der börsennotierten Leasing-Tochter abgeschafft hat.

Im Ergebnis blieb es den USA vorbehalten, der erste Markt für D&O-Versicherungen zu werden. Die Einführung dieser Versicherung ging mit dem Börsenkrach (Schwarzer Freitag) an der New Yorker Wallstreet am 25.10.1929 einher. Die damit beginnende große Rezession führte dazu, dass Banken und Unternehmen reihenweise in Konkurs gingen. Es herrschte in der Folgezeit große Verunsicherung in Wirtschaftskreisen.

Due lati della stessa medaglia

Un consiglio di amministrazione è responsabile di tutto, e il suo presidente ancora di più, secondo il principio del pars inter pares. Ovviamente non può fare tutto da se, ma avendo la responsabilità organizzativa è lui che deve rispondere. E ci sta che – come nel caso di Rupert Stadler (AUDI) – che si renda conto solo mesi dopo il suo arresto che l’accountability appartiene alla responsabilità come la farfallina alla luce.

Proprio per questo motivo gli accountable tedeschi hanno fatto i salti di gioia quando il 1.7.1994 in Germania è stata introdotta la l’assicurazione D&O I (Directors and Officers). Per controbilanciare il peso della responsabilità potevano chiedere remunerazioni stellari e pensioni di tutto rispetto, spostando la garanzia sulle compagnie di assicurazione e di re-assicurazione. Un tentativo del genere s’era già visto nella Prussia della fine dell’Ottocento. Peccato allora il ministero degli interni si oppose all’introduzione di un prodotto assicurato di così bassa leva morale.

Oggi come oggi, nelle direttive e nei codici l’unico dettaglio di interesse è il volume della franchigia. I membri di un consiglio di amministrazione devono attenersi a quelle regole che coprano anche “tutta quella roba” che gli asset manager devono fare per evitare la garanzia: chiamare una delle due grandi agenzie di “vote recommendation”, e per andare proprio sul sicuro, comprare il servizio direttamente da tutti e due – tanto, le raccomandazioni sono in genere le stessi. Il loro business – ovvero quello di farsi pagare per togliere la responsabilità all’asset manager – si complica solamente quando gli amministratori fanno delle cose (ancora) non previste dalle famose regole.

Chi glielo fa fare agli asset manager di prendersi una responsabilità (a prescindere da quella di scegliere cosa investire e disinvestire). E’ loro compito di monitorare i consigli di amministratori (e anche i board di sorveglianza) per vedere se agiscono secondo le regole dello stato, e quindi secondo la legge. Ma se è così, è difficile spiegare che ci si accontenta quando in un’assemblea generale solo due terzi dei voti sono presenti – o quando nessuno si stupisce che alla fine di un’assemblea la presenza risulta essere superiore al cento per cento.

Uno che mostra responsabilità è ad esempio la DEKA quando fa causa alla Volkswagen. Se DEKA vince, tutti gli azionisti della Volkswagen pagano il risarcimento alla DEKA dal loro patrimonio azionistico. Bastava che controllare prima e/o votare e nominare dei manager migliori. In quel caso particolare l’ironia della storia è particolarmente grottesca se ricordiamo che l’attore principale (il CFO) è stato promosso a presidente del consiglio di sorveglianza.

Allora meglio “non aver saputo niente”. Per la performance organizzativa e la competenza manageriale CdA si è messo in tasca un monte di soldi, senza svegliarsi di notte per essere a conoscenza di fatti che potrebbero tradire una colpa. L’asset manager ha (se l’ha veramente fatto) spedito i diritti di voto insieme alla garanzia comprata da ISS & Glass Lewis, senza accertarsi dove siano finiti (chiedendo una ricevuta per l’esecuzione dei voti). L’occhio non vede, cuore non duole. E a provocare il dolore in questo caso è proprio l’accountability. Però attenzione, in Germania legge introduttiva alla 2. Shareholder rights directive ha portato ad una modifica del § 129 Abs. 6 della legge sulle società quotate che dice che ogni (!) azionista ha nei confronti di un emittente il diritto ad una dichiarazione sull’effettiva esecuzione dei suoi voti – anche se al livello tecnico i limiti di questa regola si palesano al più tardi quando i voti sono andati all’estero.

Responsabilità zero, garanzia zero, e basta.

In Germania la cosiddetta Energiewende, che a dire la verità non era altro che un esproprio (anticostituzionale) degli azionisti, è stata per anni rimandata fino a che gli emittenti – oggi chiamati utility companies – si sono riorganizzati. Si, riorganizzati è proprio il termine giusto. Perché fuori dalle aziende stesse c’è stato al massimo qualche iniziativa di marketing promossa dagli asset manager che con un tenore di tipo populistico hanno fievolmente alzato la voce, invece di difendere il valore dell’azienda come unità di misura per la sostenibilità e riferimento per la loro co-determinazione. Tra i tristi esempi non ci sono E.on e RWE, Volkswagen o Daimler, ma anche la Deutsche Bank, il cui cambiamento culturale continua a scricchiolare, e ultimamente anche Thyssenkrupp. Quando alla fine le teste sono cadute, ci è voluto un po’ di tempo prima che un CdA sia riuscito mano nella mano col suo presidente scienziato a capovolgere il gruppo, pro o contro gli interessi degli azionisti. Il right of appointment (Entsenderecht) introdotto nel 2007 si mostra dal suo lato più oneroso – meno male che l’azienda di famiglia diretta da Erich SIXT ha deciso di eliminare senza sostituzione il diritto di appointment nella sua azienda di leasing (quotata).

Alla fine il primo mercato per le D&O insurances è stato quello degli Stati Uniti. L’introduzione di queste polizze è avvenuta in contemporanea con il famoso crollo della Borsa di Wall Street New Yorl il 25.10.1929, il Black Friday. La grande recessione che seguì ha fatto fallire molte banche e aziende.